According to the BVRLA, the automotive industry will experience more change in the next decade than it did in the previous 50 years.

The pace of technological development is indeed rapid and electrical and software engineers now have as pivotal a role in the industry as their mechanical cohorts.

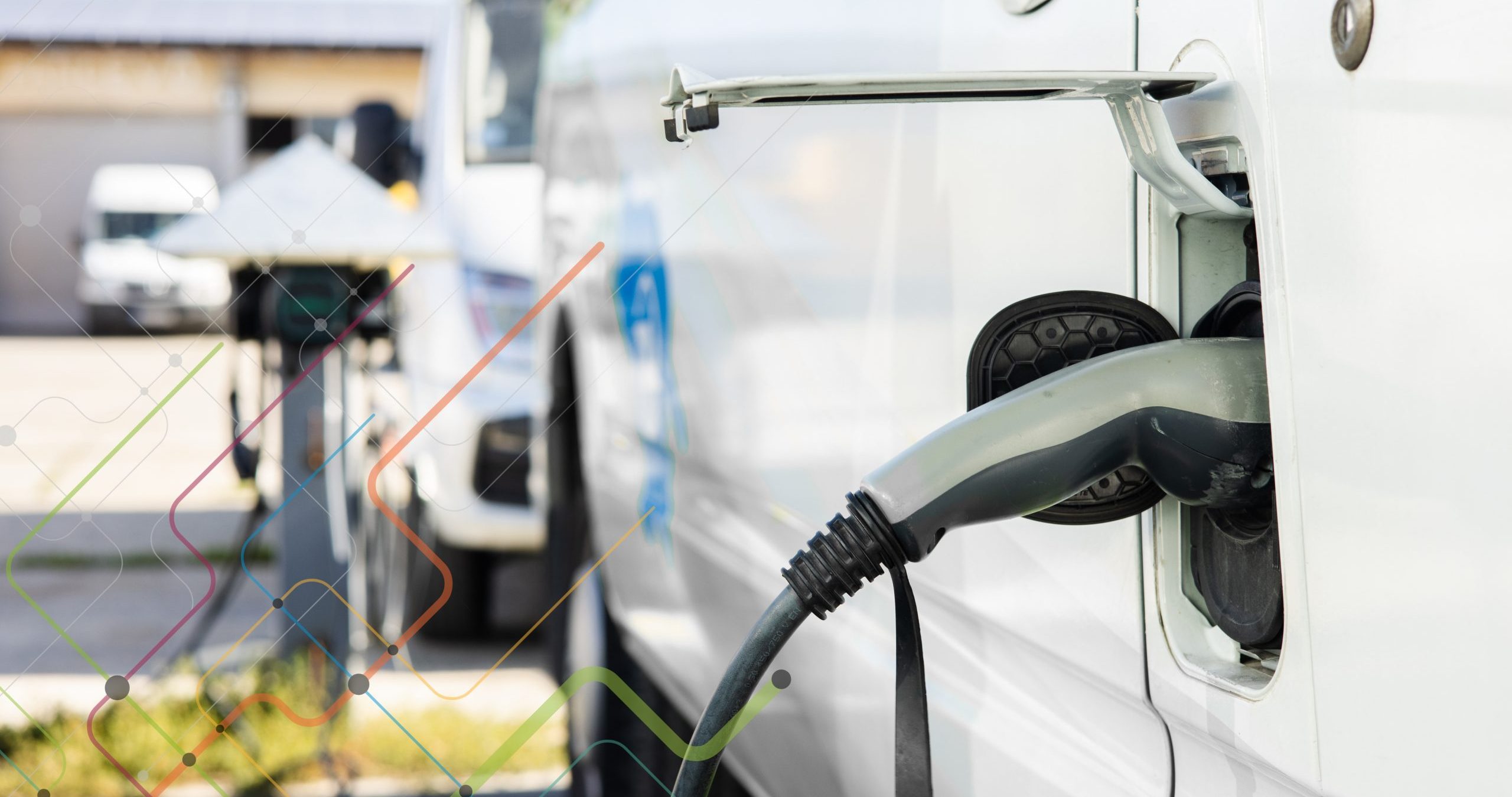

The take up of vehicles with electric powertrains continues apace and the advancement of connected car technology shows few signs of abating with industry analysts predicting every new car will have an embedded modem by 2020.

All the while, the evolution of Advanced Driver Assistance Systems (ADAS) is just as startling. Tesla vehicles, for example, are already rolling off the production line with hardware that, once activated, offers full self-driving capability.

While these developments are leading to a greener, safer driving experience for motorists and the potential for more cost-efficient fleet operations, they also pose procurement dilemmas.

A case in point might be smart, connected, navigation systems, for example, which can react to changes to drivers’ work calendars and traffic congestion in real time, while at the same time offering helpful advice such as parking space availability. Accompanying in-car tech that can notify drivers and/or fleet managers when their vehicles need servicing is now considered old news.

But the availability of new technology will increasingly call for the close scrutiny of overall costs. Fleet decision makers will need to consider various contract term options to ensure that the potential longer-term savings associated with connected systems, such as improvements in productivity, fuel economy or reduced insurance premiums have been fully assessed.

Furthermore, the automotive technology of today risks obsolescence when fleet vehicles are ready to be resold in three or four years’ time. To counter this, fleets may buck the recent trend and opt for shorter lease contracts in a bid to reduce the risk of technology becoming obsolete. The existing tech may certainly have been superseded by the next generation of advancements – the future predicted range of electric vehicles being a good example – and this, in turn, could have a significant impact on resale values of current models.

Fleet operators can already go some way to mitigating the effect of this through contract hire lease agreements, where costs are agreed up front and the leasing companies cover the risk of any potential decline in residuals.

Nevertheless, they should still be mindful of the risk of greater pressures being brought to bear on the competitiveness of rentals. Leasing providers may look to take an increasingly conservative approach to the setting of residual values on their contracts – increasing rental costs as a consequence.

Consistency is rare in the forecasting of residuals – differentials of up to £2,000 can occur among competing suppliers – and this variance can present further opportunities for fleet operators to mitigate their cost risks. Given the prevailing uncertainty and confusion around the proposed changes in CO2 and mpg calculations, a multi-supplier model may prove a particularly effective way to combat these combined threats. This model can protect businesses from the risk of being at the mercy of sole suppliers whose views of the market may be disproportionately conservative when compared to their peers.

A brave new world of fleet motoring may beckon but fleet departments must ensure they’re well placed to take a strategic approach to procurement and be ready to capitalise accordingly on the benefits that tech innovations can deliver. Advice should be sought from an outsourced specialist if the requisite expertise is not available in-house.

Read Tony’s bio here

![Carrier Transicold launches [R]eCool](https://www.fleetpoint.org/wp-content/uploads/2026/07/010-03-Carrier-Transicold-ReCool-Launch-1200x849-1-e1785319567169-100x70.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}